Coinsurance is a crucial term in the insurance industry that many people might not be fully aware of. Understanding how coinsurance works can significantly impact your insurance coverage and the amount you may need to pay out-of-pocket. In this blog post, we’ll delve into the details of coinsurance in the UK, including what it means, how it works, and why it matters for your financial security.

What is Coinsurance?

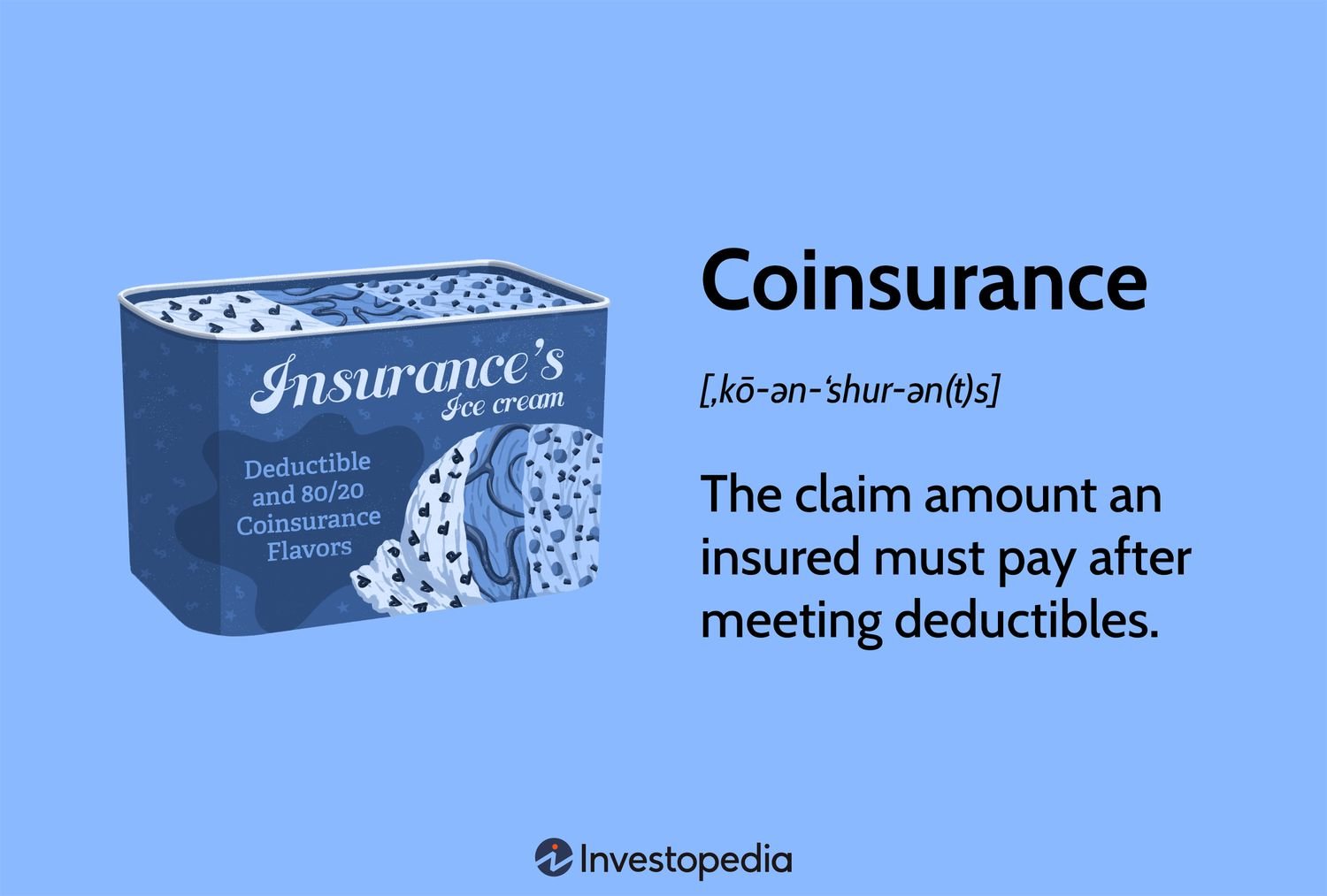

Coinsurance refers to the percentage of the cost of a claim that the policyholder must pay after exceeding their deductible. Unlike a fixed copayment, which is a specific amount paid per claim, coinsurance is typically expressed as a percentage. In the UK, coinsurance is often part of health, property, and commercial insurance policies.

For example, if your health insurance plan has a 20% coinsurance clause, this means you are responsible for paying 20% of the costs after your deductible has been met, and your insurer covers the remaining 80%.

How Does Coinsurance Work?

Coinsurance can be broken down into a simple step-by-step process:

Meet the Deductible: Before coinsurance kicks in, you must meet your policy’s deductible—the amount you must pay out-of-pocket before the insurance company starts contributing to the costs.

Split the Costs: Once the deductible is met, you and your insurer will share the remaining costs according to the coinsurance rate. For example, with a 20% coinsurance, you’ll pay 20% of each additional claim, while your insurer covers 80%.

Out-of-Pocket Maximum: Some policies have an out-of-pocket maximum, which caps the amount you need to pay in coinsurance within a specific period. Once this limit is reached, your insurer covers 100% of the costs.

Types of Insurance That Use Coinsurance

Coinsurance is commonly found in several types of insurance policies in the UK:

Health Insurance: In private health insurance plans, coinsurance is applied after meeting the deductible. It helps share the risk between you and the insurance provider, ensuring that you only pay a portion of your medical bills.

Property Insurance: Coinsurance clauses are also present in property insurance, where the policyholder must insure their property up to a certain percentage of its value. If they fail to do so, they might face penalties or reduced claim payouts.

Commercial Insurance: Businesses in the UK often have commercial insurance policies with coinsurance terms to cover property damage, liability claims, and other risks.

Pros and Cons of Coinsurance

Understanding the advantages and disadvantages of coinsurance can help you make informed decisions when choosing an insurance plan.

Pros:

Lower Premiums: Policies with coinsurance often come with lower monthly premiums compared to those with fixed copayments.

Cost Sharing: Coinsurance allows for a more balanced risk-sharing between the policyholder and the insurer.

Encourages Smart Spending: With a percentage of costs to cover, policyholders are encouraged to make more cost-effective healthcare and insurance decisions.

Cons:

Out-of-Pocket Costs: Coinsurance can lead to significant out-of-pocket expenses, especially if you have frequent or high-cost claims.

Complex Calculations: Understanding the exact amount you owe can be complicated when coinsurance rates vary depending on the type of claim.

How to Choose the Right Coinsurance Plan in the UK

Selecting the right coinsurance plan involves careful consideration of your financial situation and insurance needs. Here are a few tips to help you choose wisely:

Evaluate Your Budget: Consider how much you can afford in both monthly premiums and out-of-pocket expenses.

Check the Deductible: Policies with higher deductibles often have lower premiums but can result in higher out-of-pocket costs due to coinsurance.

Understand the Out-of-Pocket Maximum: Make sure your policy has an out-of-pocket maximum to limit your financial responsibility in the event of a costly claim.

Where to Find Coinsurance Plans in the UK

For the best coinsurance options available in the UK, it’s essential to compare different insurance providers. Websites like MoneySuperMarket and Compare the Market offer excellent resources to help you find the best deals on coinsurance and other insurance products.

Conclusion

Coinsurance is a vital aspect of many insurance policies in the UK, affecting how much you’ll pay out-of-pocket when you make a claim. Understanding how coinsurance works can help you make better financial decisions and choose the insurance plan that suits your needs. Always remember to read the fine print and compare various plans to find the best coverage for your situation.

For more detailed information about coinsurance policies, you can visit the official website of the Association of British Insurers.

Final Thoughts

If you are looking for comprehensive insurance coverage that includes coinsurance, make sure to compare different plans and providers. Understanding the ins and outs of coinsurance can help you manage your finances effectively and avoid unexpected expenses in the future.